NRB land purchase in Bangladesh is becoming a strategic priority for Non-Resident Bangladeshis (NRBs) who want to secure long-term assets in their home country. However, NRB land purchase in Bangladesh requires strict legal compliance, proper banking procedures, and structured due diligence to avoid financial and regulatory risks. At Tuhin & Partners, we provide end-to-end property advisory services tailored specifically for NRBs to ensure every land acquisition is secure, compliant, and investment-ready.

What Is NRB Land Purchase in Bangladesh?

NRB land purchase in Bangladesh refers to buying residential or commercial property by Non-Resident Bangladeshis. Agricultural land is restricted for NRBs unless inherited. Legal frameworks that govern this process include:

Why NRBs Should Invest in Bangladesh Property

-

Capital Appreciation – Urban expansion drives land value growth.

-

Rental Income – Secure steady passive income from leased properties.

-

Legacy Planning – Property for family, retirement, or inheritance.

-

Portfolio Diversification – Real estate adds stability beyond overseas investments.

Tuhin & Partners property advisory ensures your NRB investment is legally protected and structured for maximum returns.

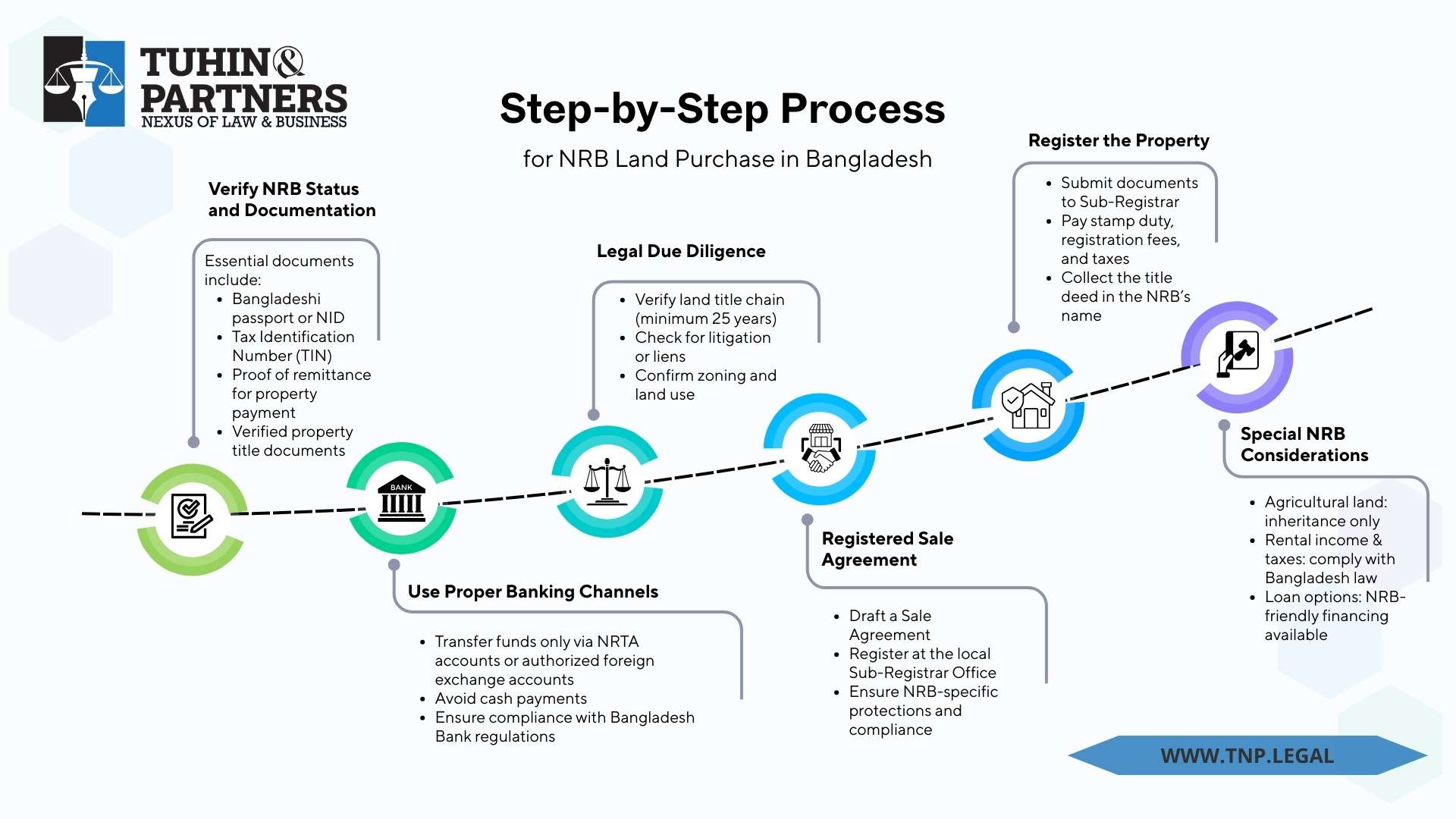

Step-by-Step Process for NRB Land Purchase in Bangladesh

Step 1 – Verify NRB Status and Documentation

Essential documents include:

-

Proof of remittance for property payment

-

Verified property title documents

Step 2 – Use Proper Banking Channels

-

Transfer funds only via NRTA accounts or authorized foreign exchange accounts

-

Avoid cash payments

-

Ensure compliance with Bangladesh Bank regulations

Step 3 – Legal Due Diligence

-

Verify land title chain (minimum 25 years)

-

Check for litigation or liens

-

Confirm zoning and land use

Tuhin & Partners conducts full legal due diligence to protect NRBs.

Step 4 – Registered Sale Agreement

-

Draft a Sale Agreement

-

Register at the local Sub-Registrar Office

-

Ensure NRB-specific protections and compliance

Step 5 – Register the Property

-

Submit documents to Sub-Registrar

-

Pay stamp duty, registration fees, and taxes

-

Collect the title deed in the NRB’s name

Step 6 – Special NRB Considerations

-

Agricultural land: inheritance only

-

Rental income & taxes: comply with Bangladesh law

-

Loan options: NRB-friendly financing available

Common Mistakes NRBs Should Avoid

-

Paying in cash

-

Skipping title verification

-

Using improper banking channels

-

Ignoring tax or mutation requirements

Tuhin & Partners property advisory helps NRBs avoid these risks.

Why Choose Tuhin & Partners?

-

Integrated Legal, Tax & Compliance Advisory

-

Led by Osman Gani Tuhin – expert in NRB property & corporate compliance

-

End-to-End Due Diligence – title verification, risk analysis, mutation support

-

NRB-Centric Services – banking compliance, inheritance structuring

-

Risk Prevention & Investment Security – avoid disputes & fraud

-

Strategic Long-Term Planning – property investment optimized for growth

Strong Ethical Standards & Transparency

Property disputes in Bangladesh often stem from:

-

Informal payments

-

Poor documentation

-

Unverified brokers

-

Missing tax records

Tuhin & Partners maintains:

-

Transparent fee structures

-

Documented compliance trails

-

Proper banking channel guidance

-

Structured advisory process

The firm does not rely on shortcuts—it builds defensible legal positions.

Strategic Vision Beyond Property

Tuhin & Partners is not just a property law firm. It positions itself as Bangladesh’s emerging legal and compliance infrastructure platform, advising clients in:

-

Corporate law

-

Investment structuring

-

Tax advisory

-

Regulatory risk

-

Commercial contracts

For NRBs who plan to invest further in Bangladesh—whether in real estate, business, or joint ventures—the relationship becomes long-term, not transactional.

FAQs – NRB Land Purchase in Bangladesh

Q1: Can NRBs legally buy land in Bangladesh?

A1: Yes, NRBs can buy residential and commercial land. Agricultural land is restricted unless inherited.

Q2: What documents do NRBs need?

A2: Passport/NID, TIN, proof of remittance, and verified property documents.

Q3: How should NRBs transfer money?

A3: Through NRTA accounts or authorized foreign exchange accounts. Avoid cash.

Q4: Do NRBs need to register the property?

A4: Yes, registration at the Sub-Registrar Office is mandatory.

Q5: Can NRBs get loans to buy property?

A5: Yes, many banks provide NRB-specific loans with equity requirements.

Q6: Why hire Tuhin & Partners?

A6: End-to-end legal, tax, and compliance advisory tailored for NRBs.

Q7: What mistakes should NRBs avoid?

A7: Paying in cash, skipping title verification, ignoring taxes, and using improper banking channels.