Bangladesh, one of South Asia’s fastest-growing economies, continues to attract substantial foreign direct investment (FDI) due to its liberal investment regime, strategic location, and competitive labour costs. A critical consideration for foreign investors is the repatriation of profits, capital, and disinvestment proceeds. This article provides a comprehensive guide to the legal procedures, regulatory framework, practical steps, and challenges associated with the Repatriation of Profits and Investments in Bangladesh.

Legal Framework for Repatriation of Profits And Investments In Bangladesh

The right to repatriate profits and investments is protected by national legislation and supported by international treaties and bilateral investment agreements.

Key Laws and Regulations for Repatriation of Profits And Investments In Bangladesh

- Foreign Private Investment (Promotion and Protection) Act, 1980

- Foreign Exchange Regulations Act, 1947

- Guidelines for Foreign Exchange Transactions (GFET)

- Income Tax Act, 2023

- Bangladesh Investment Development Authority (BIDA) Act, 2016

- One Stop Service Act, 2018

These laws collectively guarantee non-discriminatory treatment for foreign investors and allow for the repatriation of:

- Dividends and profits

- Salaries and savings of expatriates

- Sale proceeds from shares and disinvestment

- Royalties and technical fees

- Capital gains and interest on foreign loans

Eligibility and Preconditions for Repatriation of Profits And Investments In Bangladesh

To legally repatriate funds, foreign investors must fulfil several conditions:

- Investment Registration

All foreign equity investments must be registered with BIDA. - Documentary Compliance

Repatriation requests must be backed by audited financials, tax clearance certificates, and proper banking records. - Tax Clearance

All applicable taxes—including corporate tax, capital gains tax, and withholding tax—must be fully paid. - Use of Authorized Dealer (AD) Banks

Only licensed commercial banks designated as Authorized Dealers may process repatriation under supervision from Bangladesh Bank.

Categories of Repatriable Funds

1. Dividends and Profit Repatriation

Foreign shareholders may repatriate net dividends after:

- Deducting a 20% withholding tax (subject to Double Taxation Agreements)

- Submitting board resolutions, audited accounts, and evidence of dividend declaration

2. Disinvestment and Capital Repatriation

Upon sale or transfer of shares:

- A foreign investor may repatriate the sale proceeds after tax adjustment

- Valuation must be conducted by an independent chartered accountant or merchant banker

3. Royalty, Franchise, and Technical Fees

These payments are repatriable only if:

- The underlying agreement is approved by BIDA

- The total fee does not exceed 6% of the annual turnover unless otherwise justified

4. Loan Repayments and Interest

Foreign loans approved by the Bangladesh Bank can be serviced and repatriated. Approval typically covers:

- Principal repayment schedule

- Interest rate and fees

- Grace period and tenor

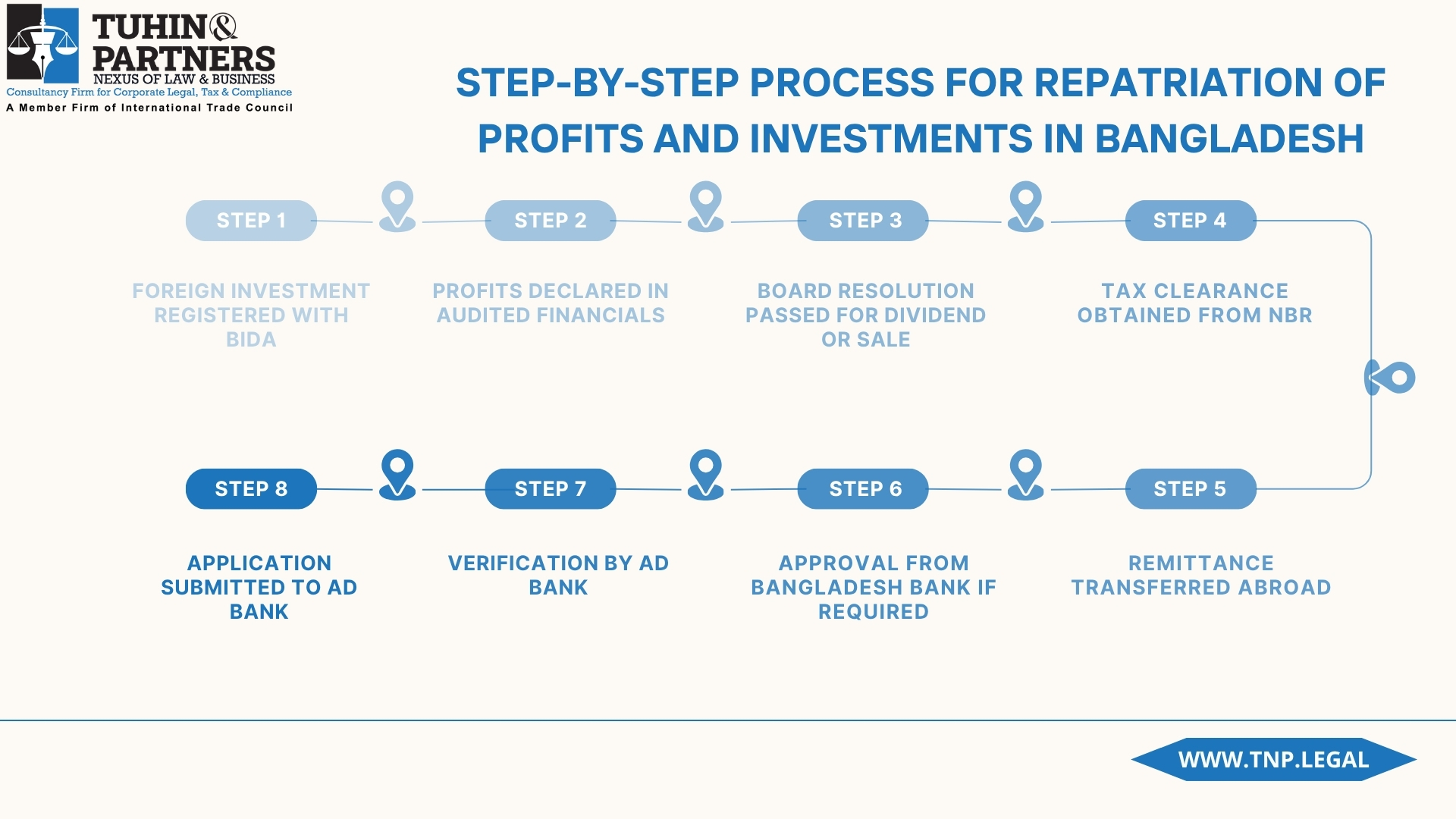

Step-by-Step Process for Repatriation of Profits And Investments In Bangladesh

Role of Bangladesh Bank and BIDA for Repatriation of Profits And Investments In Bangladesh

Bangladesh Bank

- Monitors foreign exchange transactions

- Requires prior approval for certain high-value or sensitive remittances

- Maintains data on remittance flows and FDI

BIDA

- Registers foreign investments

- Approves technical assistance and royalty agreements

- Acts as a one-stop service centre for investor facilitation

Tax Implications of Repatriation for Profits And Investments In Bangladesh

Understanding the tax regime is critical for efficient fund repatriation:

| Type of Income | Applicable Tax | Notes |

|---|---|---|

| Dividends | 20% Withholding Tax | May be reduced under Double Taxation Avoidance Treaties |

| Capital Gains | 15% (non-resident) | Based on differential between sale and cost |

| Royalty/Tech Fees | 20% Withholding Tax | Subject to BIDA approval |

| Interest on Loans | 20% Withholding Tax | Tax treaties may provide relief |

Foreign investors are advised to consult tax professionals to leverage Double Taxation Avoidance Agreements (DTAAs) for tax optimization.

Common Challenges and Practical Tips for Repatriation of Profits And Investments In Bangladesh

Challenges

- Delays in Tax Clearance from the National Board of Revenue (NBR)

- Currency convertibility issues during macroeconomic shocks

- Regulatory ambiguity on disinvestment valuation

- Frequent changes in tax and banking circulars

Practical Tips

- Ensure early BIDA registration and approval of service agreements

- Maintain clear and auditable documentation

- Engage with reputed chartered accountants and tax advisors

- Work closely with Authorized Dealer banks with international transaction experience

Recent Developments and Reforms

- Bangladesh Bank Circular (2023) enabled the repatriation of capital gains without prior approval if within specified thresholds

- BIDA OSS Portal (One Stop Service) has streamlined approval and registration processes

- Digital tax return and clearance system implemented to reduce delays

Conclusion

Bangladesh offers an increasingly investor-friendly regime for repatriating profits and investments. However, compliance with regulatory formalities, proactive tax planning, and diligent documentation are essential. Foreign investors are strongly encouraged to engage legal, tax, and financial advisors to ensure a smooth repatriation process aligned with national laws and international standards.

Need Expert Help?

Tuhin & Partners assist foreign investors with end-to-end support—from BIDA registration and agreement structuring to tax clearance and fund repatriation. Reach out today to ensure your investments are secure and your profits are repatriated legally and efficiently.

FAQs on Repatriation of Profits And Investments In Bangladesh

How Outward Remittances are Regulated in General in Bangladesh?

Bangladesh Bank (BB) regulates outward remittance. The following outward remittances can be made with prior approval of BB;

- Dividend,

- Training and consultancy fees,

- Repayment of approved foreign loans. On the other hand, specific guidance and conditions have been prescribed for the following remittances:

- Royalty, franchise, technical license/ know-how/ assistance fees,

- Transfer of shares and securities.

Specific foreign exchange regulations are in force for the particular businesses, including shipping agents, freight forwarding agents, courier companies and airline companies.

What is the Procedure for Outward Remittances of Dividend, Profit, etc.?

• Dividend income (both final and interim) can be remitted through an authorized dealer of the non-resident shareholders. The application must be made in the prescribed form and certified by an auditor.

• Remittable dividend can be credited to foreign currency accounts maintained by the non-resident shareholders as per FE Circular No.29 (Jul. 2020) of Bangladesh Bank. Profits:

• Branch offices of foreign companies, banking and insurance institutions incorporated in Bangladesh can remit post-tax profits to the head offices through an authorized dealer. However, branch offices other than banks and insurance need permission from BIDA and Bangladesh Bank to remit profits.

•Repatriation of savings, retirement benefits and salary of expatriate employees: Foreigners employed in Bangladesh can remit 75% of their monthly salary after deducting all admissible expenses, savings and admissible retirement benefits through an authorized dealer.